Whether you’re applying for a mortgage, personal loan, student loan, or small business loan, lender borrowing criteria are the gatekeepers standing between you and your financing. These are the specific financial standards that banks, credit unions, mortgage companies, and government-backed lenders use to decide if you’re a trustworthy borrower.

Understanding lender borrowing criteria before you apply can make the difference between approval and rejection — or between a competitive interest rate and a costly one. This guide breaks down exactly what lenders look for, how each factor is evaluated, and what you can do to strengthen your application.

We cover the full underwriting process from credit scores and income verification to debt-to-income ratios and asset liquidity. Whether you’re a first-time homebuyer, a student exploring loan options, or a business owner applying for an SBA loan, this article gives you the practical knowledge to move forward with confidence.

What Is Lender Borrowing Criteria?

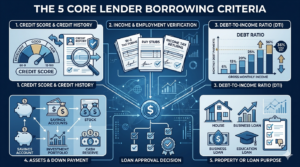

Lender borrowing criteria vary depending on the type of loan, the lender, and whether the loan is conventional, government-backed, or commercial. However, most lenders evaluate borrowers across five core areas: credit history, income and employment, debt-to-income ratio, assets, and the property or purpose of the loan

The 5 Core Lender Borrowing Criteria

Lenders use a structured underwriting process to evaluate risk. While specific thresholds vary by lender and loan type, five criteria form the foundation of nearly every loan decision in the United States.

1. Credit Score and Credit History

Your credit score — most commonly a FICO score is one of the most influential factors in any lending decision. FICO scores range from 300 to 850. Most conventional mortgage lenders require a minimum FICO score of 620, while FHA loans may allow scores as low as 500 with a larger down payment.

The three major credit bureaus — Equifax, TransUnion, and Experian — each generate credit reports. Mortgage lenders typically pull all three and use the middle score. Lenders review not just your score but the underlying history: payment record, length of credit history, credit mix, new inquiries, and amounts owed.

According to FICO, payment history accounts for 35% of your score, making on-time payments the single most important factor. Amounts owed (credit utilization) makes up 30%.

2. Income and Employment Verification

Lenders need to confirm that you earn enough money, and that your income is stable and likely to continue. This is called verifiable income, and it forms the basis for assessing repayment capacity.

Typical documentation includes:

- Recent pay stubs (typically two months)

- W-2 forms from the past two years

- Federal tax returns (especially for self-employed borrowers)

- Bank statements

- Profit and loss statements for business owners

Self-employed borrowers often face stricter scrutiny. Lenders may require two years of tax returns filed with the Internal Revenue Service (IRS) and calculate income using net profit rather than gross revenue.

Fannie Mae guidelines, which govern conventional conforming loans, require lenders to document income with precision. Employment gaps, recent job changes, or irregular income may trigger additional review.

3. Debt-to-Income Ratio (DTI)

Your debt-to-income ratio measures how much of your gross monthly income goes toward existing and new debt payments. It is one of the most important indicators of borrower solvency.

DTI is calculated as: Total Monthly Debt Payments / Gross Monthly Income x 100

Lenders evaluate two DTI figures:

- Front-end DTI: Only housing costs (mortgage principal, interest, taxes, insurance) divided by gross income. Most conventional lenders prefer this below 28%.

- Back-end DTI: All monthly debts (housing + car loans + student loans + credit cards + other obligations) divided by gross income. Most conventional lenders prefer this below 36-43%.

Fannie Mae and Freddie Mac allow DTI ratios up to 45-50% in some cases with compensating factors. FHA loans allow up to 57% back-end DTI in certain circumstances, though lender overlays often apply stricter limits.

4. Assets and Down Payment

Lenders evaluate your asset liquidity — the money and resources you have available to cover the down payment, closing costs, and financial reserves after closing. Having reserves demonstrates financial stability and reduces lender risk.

For conventional loans, a 20% down payment eliminates the need for private mortgage insurance (PMI). However, borrowers can qualify with as little as 3% down through programs like Fannie Mae’s HomeReady or Freddie Mac’s Home Possible.

FHA loans require as little as 3.5% down with a credit score of 580 or higher. VA loans and USDA loans offer zero down payment options for eligible borrowers.

Assets can include:

- Checking and savings accounts

- Investment accounts (stocks, bonds, mutual funds)

- Retirement accounts (often counted at 60-70% of value)

- Gift funds (with documentation requirements)

- Proceeds from sale of existing property

5. Property or Loan Purpose

For mortgage loans, the property itself must meet certain standards. An independent appraiser assesses the home’s market value, and lenders will not lend more than the property is worth (loan-to-value ratio or LTV must meet program limits).

For SBA loans through the Small Business Administration, the purpose of the loan and how the funds will be used are closely scrutinized. The business must operate for profit, meet SBA size standards, and demonstrate a need for the financing.

How to Prepare for Lender Borrowing Criteria: Step by Step

Follow these steps before submitting any loan application to maximize your chances of approval and secure the best possible terms.

- Pull Your Credit Reports — Request free credit reports from all three bureaus at AnnualCreditReport.com. Review for errors, disputed accounts, or outdated negative items.

- Check Your FICO Score — Many banks and credit card companies offer free FICO scores. Know your score and understand which tier you fall in before applying.

- Calculate Your DTI — Add up all monthly debt obligations and divide by your gross monthly income. If your back-end DTI exceeds 43%, work on paying down debt before applying.

- Gather Income Documentation — Collect recent pay stubs, W-2s, tax returns, and bank statements. Self-employed borrowers should prepare business tax returns and a P&L statement.

- Assess Your Assets — Calculate available funds for down payment and reserves. Ensure funds have been in your accounts for at least 60 days (lenders call this ‘seasoned’ funds).

- Reduce New Credit Inquiries — Avoid opening new credit accounts or making large purchases on credit in the 90 days before applying, as new inquiries can temporarily lower your score.

- Get Pre-Qualified Then Pre-Approved — A pre-qualification assessment gives you a general sense of eligibility. A pre-approval involves full verification and carries more weight with sellers and lenders.

- Compare Multiple Lenders — Different lenders have different overlays (internal requirements stricter than minimum guidelines). Banks like Bank of America and Wells Fargo may have different standards than credit unions or online lenders.

- Work with a HUD-Approved Housing Counselor (if needed) — If your credit or income is borderline, a HUD-approved counselor can help you create a plan to qualify.

Lender Borrowing Criteria by Loan Type: Comparison Table

| Loan Type | Min. Credit Score | Max DTI | Min. Down Payment | Key Governing Body |

| Conventional | 620 (typical) | 45-50% (with compensating factors) | 3-20% | Fannie Mae / Freddie Mac |

| FHA Loan | 500 (10% down) / 580 (3.5% down) | Up to 57% (lender limits apply) | 3.5% | FHA / HUD |

| VA Loan | No official minimum (lender sets) | 41% preferred (flexible) | 0% | VA / Department of Veterans Affairs |

| USDA Loan | 640 (recommended) | 41% (back-end) | 0% | USDA Rural Development |

| SBA 7(a) Loan | Varies (typically 650+) | Debt Service Coverage Ratio reviewed | Varies (10-30%) | Small Business Administration |

| SBA 504 Loan | Varies (typically 650+) | DSCR 1.25x minimum | 10% typical | Small Business Administration |

| Jumbo Loan | 700-720+ (varies by lender) | 43% or lower | 10-20%+ (varies) | Private lenders / no GSE backing |

| Student Loans (Federal) | No minimum (Direct Loans) | N/A (income-driven repayment) | N/A | Federal Student Aid / Dept. of Education |

| Commercial Real Estate | 680+ (varies) | DSCR 1.25x+ standard | 20-35% typical | Private lenders / SBA / banks |

The Underwriting Process: How Lenders Evaluate Your Application

Underwriting is the formal process through which a lender’s team reviews, verifies, and risk-assesses your loan application. Understanding what happens behind the scenes can help you respond quickly to requests and avoid common delays.

Automated Underwriting Systems (AUS)

Most lenders first run your application through an automated underwriting system. Fannie Mae’s Desktop Underwriter (DU) and Freddie Mac’s Loan Product Advisor (LPA) are the two most widely used systems. These tools instantly analyze your credit, income, and assets against the lender’s guidelines and return an Approve/Eligible, Refer, or Refer with Caution result.

Manual Underwriting

If the AUS returns a Refer decision, or if your loan doesn’t fit standard parameters (non-QM loans, certain FHA scenarios), a human underwriter reviews your file manually. This is common for self-employed borrowers or those with complex financial situations. Manual underwriting relies heavily on compensating factors — positive financial traits that offset risk.

Conditions and Suspense

Even after initial approval, underwriters typically issue conditions — additional documentation or explanations required before final approval. Common conditions include:

- Letter of explanation for credit inquiries

- Documentation of large deposits

- Updated pay stubs or bank statements

- Proof of homeowner’s insurance

- Appraisal review and property clearance

CFPB and Consumer Protections

The Consumer Financial Protection Bureau (CFPB) oversees how lenders handle applications. Under the Equal Credit Opportunity Act (ECOA), lenders cannot discriminate based on race, color, religion, sex, national origin, age, marital status, or because you receive public assistance. If denied, lenders must provide a written adverse action notice explaining the reasons.

Credit Score Requirements: What You Need to Know

Credit scoring is one of the most misunderstood parts of the borrowing process. Here’s a clear breakdown of what lenders see and how it affects your loan terms.

FICO Score Ranges and What They Mean for Borrowers

| FICO Score Range | Category | Likely Impact on Borrowing |

| 800-850 | Exceptional | Best available rates; highest approval likelihood |

| 740-799 | Very Good | Strong rates; easy qualification for most loans |

| 670-739 | Good | Average rates; qualifies for most conventional products |

| 580-669 | Fair | Higher rates; may need FHA or subprime options |

| 500-579 | Poor | Limited options; FHA with 10% down; high rates |

| Below 500 | Very Poor | Most traditional lenders will decline; limited alternatives |

Borrowing Criteria for Specific Loan Types

Mortgage Loans

Conventional mortgage lenders follow guidelines set by Fannie Mae and Freddie Mac. These include specific requirements on loan-to-value ratios, borrower income stability, and amortization schedules. The conforming loan limit for 2024 is $766,550 for single-family homes in most U.S. counties (higher in designated high-cost areas).

Lenders calculate your amortization schedule to ensure the loan is fully paid off by the end of the term. A standard 30-year fixed mortgage amortizes over 360 payments, with early payments weighted heavily toward interest.

SBA Loans

The Small Business Administration guarantees SBA loans made by approved lenders. The SBA 7(a) loan program is the most common. To qualify, businesses must:

- Operate for profit in the United States

- Meet SBA size standards (typically fewer than 500 employees for most industries)

- Demonstrate a reasonable need for the loan

- Have good character (criminal background review included)

- Show an inability to obtain the same financing elsewhere on reasonable terms

SBA lenders evaluate debt service coverage (DSCR) — the ratio of net operating income to total debt service. A DSCR of 1.25x or higher is typically required, meaning the business generates $1.25 for every $1 of debt payment.

Student Loans

Federal student loans (Direct Subsidized, Unsubsidized, and PLUS loans) are administered through Federal Student Aid and do not require a credit score check for undergrad Direct Loans. Graduate PLUS and Parent PLUS loans require no adverse credit history.

Private student loans, however, follow traditional lender borrowing criteria: credit score, income (or a co-signer’s income), and enrollment status. Interest rates on private loans vary widely based on creditworthiness.

Commercial Loans

Commercial real estate and business loans are evaluated differently from consumer loans. Key criteria include:

- Debt Service Coverage Ratio (DSCR): Typically 1.25x minimum

- Loan-to-Value (LTV): Usually 65-80% maximum

- Business financials: Three years of business tax returns

- Global cash flow analysis: Personal and business income combined

- Collateral quality: Type, condition, and marketability of the property or assets

Common Mistakes Borrowers Make (And How to Avoid Them)

- Applying Without Knowing Your Credit Score: Many borrowers apply cold, not knowing their score is below the lender’s minimum. Pull your reports and score 90-120 days before applying so you have time to correct errors or improve.

- Ignoring Debt-to-Income Ratio: Focusing only on credit score while ignoring DTI is a common error. Even with excellent credit, a DTI above 50% can lead to denial. Pay down revolving debt before applying.

- Making Large Purchases Before Closing: Buying a car, opening a new credit card, or taking on any new debt between pre-approval and closing can change your DTI and credit score — potentially killing the loan.

- Changing Jobs at the Wrong Time: Lenders want to see stable employment. Changing jobs — especially industries — shortly before or during the loan process can trigger additional scrutiny or cause delays.

- Moving Money Without Documentation: Large, unexplained deposits in your bank accounts raise red flags. Lenders need to trace all large deposits. If you receive gift funds, get a proper gift letter as required by lender guidelines.

- Assuming Pre-Qualification Equals Pre-Approval: Pre-qualification is a soft estimate. Pre-approval involves actual credit checks, income verification, and carries far more weight. Don’t assume pre-qualification is sufficient for making serious purchase offers.

- Only Comparing Rates, Not Terms: A lower interest rate with higher fees can cost more over time. Compare APR (annual percentage rate), closing costs, loan term, prepayment penalties, and other conditions — not just the advertised rate.

- Not Exploring Government-Backed Programs: Many borrowers with average credit assume conventional loans are their only option. FHA, VA, USDA, and SBA programs offer more flexible criteria and can save significant money.

Final Conclusion :

Understanding lender borrowing criteria is not just helpful — it’s essential for anyone who wants to borrow money in today’s financial environment. From FICO credit scores evaluated by Equifax, TransUnion, and Experian, to income verification guided by IRS documentation requirements, to DTI ratios governed by Fannie Mae and Freddie Mac guidelines, every piece of criteria has a clear purpose: to assess whether you can and will repay what you borrow.

The good news is that these criteria are not arbitrary. They are measurable, manageable, and improvable. By knowing where you stand, gathering the right documentation, reducing existing debt, and choosing the right loan product — whether conventional, FHA, VA, USDA, SBA, or student loan — you put yourself in the strongest possible position before your application is ever reviewed by an underwriter.

If you have questions about your specific situation, consult a HUD-approved housing counselor, a licensed mortgage professional, or a financial advisor. The Consumer Financial Protection Bureau (CFPB) also offers free educational resources and tools to help borrowers make informed decisions.