Most homeowners make their monthly mortgage payment without fully understanding where that money goes. The answer lies in how mortgage amortization works — a structured debt liquidation process that determines exactly how each dollar of your payment is split between interest and loan principal across the entire life of your loan.

Understanding mortgage amortization is not just academic. It affects how much total interest you pay, how quickly you build equity, whether extra payments make sense, and how refinancing decisions should be evaluated. For first-time buyers especially, grasping this concept before signing a loan changes how you approach every payment you’ll make.

This guide explains exactly how the amortization process works, walks through the math step by step, shows you a real amortization schedule example, covers negative amortization risk, and explains how different loan types and strategies interact with the reducing balance method. By the end, you’ll have a clear picture of your mortgage from day one to the loan maturity date.

The word ‘amortization’ comes from the Latin ‘amortire’ — meaning to kill off or extinguish. In mortgage terms, it means systematically extinguishing a debt through regular payments using the reducing balance method.

Each periodic installment in a fully amortizing loan is identical in size (for fixed-rate mortgages), but the allocation between interest and principal changes with every payment. This shifting allocation is the core mechanism of mortgage amortization, and it has significant implications for equity accumulation and total interest cost.

How Mortgage Amortization Works: The Core Mechanics

The Interest-Heavy Early Years

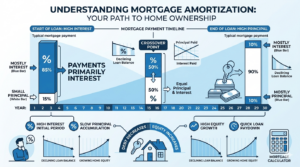

The most important thing to understand about mortgage amortization is the interest-heavy early years. Because interest is calculated on the outstanding balance — and that balance is highest at the beginning — the first years of your mortgage are dominated by interest payments.

On a 30-year fixed mortgage, the typical borrower pays far more in interest than in principal during the first decade. This is not a lender trick; it is a mathematical consequence of how compound interest effects work on a large, slowly declining balance.

Example: On a $300,000 mortgage at 7% interest over 30 years, the monthly payment is approximately $1,996. In Month 1, roughly $1,750 goes to interest and only $246 goes to principal. By Month 180 (Year 15), the split has shifted to roughly $1,250 interest and $746 principal. By Month 340 (Year 28), the majority of each payment is reducing the balance.

The Reducing Balance Method Explained

The reducing balance method (also called the declining balance method) calculates interest only on the remaining loan balance, not the original loan amount. This is why interest costs decrease gradually as you pay down the principal.

Each month:

- Your lender calculates interest by multiplying the current outstanding balance by the monthly interest rate (annual rate / 12).

- The interest amount is subtracted from your fixed payment.

- The remainder reduces the principal balance.

- The next month’s interest is calculated on the new, lower balance.

This cycle repeats every month until the balance reaches zero the loan maturity date.

Payment Allocation Over Time

Payment allocation describes how your fixed monthly payment is split between interest and principal at any given point in the loan term. In early years, the ratio is heavily weighted toward interest. In later years, it shifts heavily toward principal reduction.

This pattern explains why:

- Selling or refinancing in the first 5-7 years means you have built relatively little equity through principal payments.

- Making even one extra principal payment early in the loan has an outsized impact on total interest paid.

- The straight-line vs declining balance distinction matters most US mortgages use the declining balance method, not a straight-line split.

Equity Accumulation Through Amortization

Equity accumulation through amortization is the gradual increase in the portion of your home you own outright. Your equity is the difference between the home’s market value and your outstanding loan balance.

Amortization builds equity slowly at first and faster later. However, equity also grows when home values appreciate — which is separate from the amortization process. Falling home values can reduce equity even when you are making payments on time.

Understanding the pace of equity accumulation helps borrowers decide when to refinance, whether to make extra payments, and whether a home equity loan or line of credit is accessible.

The Mortgage Amortization Formula

The fixed monthly payment for a fully amortizing mortgage calculator using this standard formula:

Example calculation: $300,000 loan, 7% annual rate, 30-year term

- P = $300,000

- r = 0.07 / 12 = 0.005833

- n = 30 x 12 = 360

- M = 300,000 x [0.005833 x (1.005833)^360] / [(1.005833)^360 – 1]

- M = approximately $1,996 per month

Over the full 360 payments, total payments equal roughly $718,560 — meaning the total interest paid on this loan is approximately $418,560. This illustrates the compound interest effects of a long-term mortgage and underscores why interest rate and loan term decisions are so consequential.

The Truth in Lending Act (TILA), enforced by the Consumer Financial Protection Bureau (CFPB), requires lenders to disclose the total interest you will pay over the full loan term in your Loan Estimate and Closing Disclosure documents. Review these figures carefully before closing.

How to Read and Use a Mortgage Amortization Schedule: Step by Step

An amortization schedule is a full table showing every payment from loan origination to the loan maturity date. Here is how to read and use it effectively.

- Obtain Your Amortization Schedule — Request your full amortization schedule from your lender at closing, or generate one using Bankrate’s mortgage calculator, Rocket Mortgage’s online tools, or Microsoft Excel Amortization Templates available from Microsoft’s template library.

- Identify the Four Columns — Every amortization schedule has four core columns: Payment Number (or Date), Beginning Balance, Payment Amount (broken into Interest and Principal), and Ending Balance. Locate these in your schedule.

- Review Month 1 — Look at the first payment row. Note how much goes to interest vs. principal. This ratio is highest in favor of interest at the very start and will gradually reverse over the loan term.

- Find the Crossover Point — The crossover point is where your principal payment exceeds your interest payment for the first time. On a 30-year loan at typical rates, this usually occurs somewhere between Year 18 and Year 22. Locate this row in your schedule.

- Calculate Equity at Key Milestones — Look at the Ending Balance column at Year 5, Year 10, and Year 15. Subtract each from your original purchase price to see how much principal you will have repaid by those dates. Compare to your home’s estimated value to see projected equity.

- Identify the Impact of Extra Payments — Many amortization calculators allow you to add extra principal payments. Try adding $100 or $200 per month in extra principal and see how many months the loan shortens and how much total interest you save. This models the impact of principal reduction decisions.

- Locate Total Interest Paid — At the bottom of your amortization schedule, you will find total interest paid over the full term. Compare this to your original loan amount to understand the true cost of borrowing.

- Compare with Your TILA Disclosures — Cross-reference your amortization schedule with the Total of Payments and Finance Charge figures on your Loan Estimate or Closing Disclosure. These are required TILA disclosures that confirm the total interest cost of your loan.

- Revisit When Considering Refinancing — When evaluating a refinance, compare where you are on your current amortization schedule to what a new schedule would look like. Restarting a 30-year amortization resets the interest-heavy early years, which may cost more even if the rate is lower.

Mortgage Amortization: Sample Payment Allocation Over 30 Years

The table below shows how payment allocation shifts between interest and principal on a $300,000 mortgage at 7% annual interest over a 30-year term. Monthly payment is approximately $1,996. Figures are rounded for clarity.

| Payment Year | Approx. Monthly Interest | Approx. Monthly Principal | Remaining Balance | Equity Built (Principal Only) |

| Year 1 (Month 1) | $1,750 | $246 | $299,754 | $246 |

| Year 3 (Month 36) | $1,693 | $303 | $290,172 | $9,828 |

| Year 5 (Month 60) | $1,628 | $368 | $279,163 | $20,837 |

| Year 10 (Month 120) | $1,453 | $543 | $249,017 | $50,983 |

| Year 15 (Month 180) | $1,248 | $748 | $213,806 | $86,194 |

| Year 20 (Month 240) | $1,003 | $993 | $171,494 | $128,506 |

| Year 25 (Month 300) | $704 | $1,292 | $119,843 | $180,157 |

| Year 28 (Month 336) | $490 | $1,506 | $83,348 | $216,652 |

| Year 30 (Month 360) | $12 | $1,984 | $0 | $300,000 |

How Different Mortgage Types Affect Amortization:

Fixed-Rate Mortgages

Fixed-rate mortgages have the most straightforward amortization. The interest rate never changes, so the payment amount stays the same throughout the loan term. Only the allocation between interest and principal shifts each month. The Government National Mortgage Association (Ginnie Mae), Fannie Mae, and Freddie Mac all back pools of fixed-rate mortgages as the foundation of the US mortgage market.

Adjustable-Rate Mortgages (ARMs)

Adjustable-rate mortgages (ARMs) have fixed payments for an initial period (commonly 5, 7, or 10 years), after which the rate adjusts periodically based on a benchmark index. When the rate adjusts, the remaining loan balance is re-amortized at the new rate — meaning a new payment is calculated to pay off the remaining balance over the remaining term. This can increase or decrease your payment significantly.

FHA, VA, and USDA Loans

FHA loans (insured by the Federal Housing Administration), VA loans (guaranteed by the Department of Veterans Affairs), and USDA loans all use standard amortization schedules for their fixed-rate products. The amortization mechanics are identical to conventional loans. The primary differences are in mortgage insurance requirements, eligibility, and down payment rules — not the amortization structure.

Negative Amortization Risk

Negative amortization occurs when your monthly payment is less than the interest owed in a given period. Instead of the balance declining, it grows — defeating the purpose of debt liquidation. This is a risk associated with certain loan types including payment-option ARMs, deferred-interest loans, and some income-driven repayment structures.

The CFPB’s Qualified Mortgage (QM) rules generally prohibit negative amortization features in QM loans. However, non-QM loans and older loan products may still carry this risk. Borrowers should confirm their loan is fully amortizing before signing.

Interest-Only Loans

Interest-only loans require only interest payments for a fixed initial period (typically 5-10 years). During this time, the balance does not decrease — no principal reduction occurs and no equity accumulates through payments. After the interest-only period ends, the loan re-amortizes over the remaining term, often resulting in a significantly higher monthly payment.

How Extra Payments Accelerate Amortization

Making additional principal payments above your scheduled payment is one of the most effective ways to reduce total interest paid and shorten the loan term. Because interest is calculated on the remaining balance each month, reducing that balance faster has a compounding positive effect.

Example: On the $300,000 mortgage at 7% for 30 years, making an additional $200/month in principal payments from Month 1 could save approximately 5-6 years of payments and tens of thousands of dollars in total interest, depending on exact timing and rates. Use an amortization calculator (available on Bankrate or via Microsoft Excel Amortization Templates) to model your specific scenario.

Key rules for extra payments:

- Confirm with your lender that extra payments are applied directly to principal — not held for the next payment.

- Check your loan documents for prepayment penalty clauses. Most conventional loans have no prepayment penalty, but some mortgages — particularly certain non-QM loans — may.

- Extra payments made in early years have the greatest impact on total interest saved because they reduce the base on which all future interest is calculated.

Common Mistakes Borrowers Make About Mortgage Amortization

- Not Reviewing the Amortization Schedule Before Closing: Many borrowers never ask for or review their full amortization schedule. Seeing the total interest figure — often equal to or greater than the original loan — motivates better financial decisions about loan term, extra payments, and refinancing.

- Focusing Only on Monthly Payment, Not Total Interest: A lower monthly payment from a 30-year term vs. a 15-year term looks appealing, but the 30-year loan can cost twice as much in total interest. Always compare total interest paid — not just monthly payment — when choosing a loan term.

- Refinancing Without Accounting for Amortization Reset: Refinancing resets your amortization schedule. If you are 8 years into a 30-year loan and refinance into a new 30-year loan, you restart 30 years of amortization. Even at a lower rate, you may pay more total interest unless you refinance into a shorter remaining term.

- Assuming All Payments Build Equity Equally: Borrowers often assume each payment builds the same amount of equity. In reality, equity accumulates slowly at first and accelerates later. Expecting significant equity after just 3-4 years of payments can lead to disappointment or poor financial decisions.

- Ignoring Negative Amortization Risk on Adjustable Loans: Payment-option ARM products can allow borrowers to make minimum payments that do not cover interest, causing the balance to grow. Always verify that your loan is fully amortizing and understand what happens to your payment after any initial fixed period.

- Not Understanding How PMI Interacts with Amortization: Private mortgage insurance (PMI) is required when your loan-to-value (LTV) ratio exceeds 80%. As amortization reduces your balance, your LTV drops. Once you reach 80% LTV, you may request PMI cancellation — a significant monthly savings. Track your amortization schedule to know when to make this request.

- Misreading TILA Disclosures: The Truth in Lending Act (TILA) requires disclosure of the Annual Percentage Rate (APR), total of payments, and finance charge on your Closing Disclosure. Some borrowers focus only on the interest rate, missing the APR (which includes fees) and the total interest cost shown in these required disclosures.

Final Conclusion

Understanding how mortgage amortization works transforms the way you think about your home loan. Every payment you make is not just a bill — it is a step in a structured debt liquidation process that gradually shifts from financing the lender’s profit (interest) to building your own wealth (equity accumulation).

The interest-heavy early years are not a flaw in the system; they are a mathematical consequence of borrowing a large sum at interest over time using the reducing balance method. What matters is that you understand the pattern, use it to your advantage, and make informed decisions about extra payments, refinancing, loan term selection, and PMI removal.

Resources from the Consumer Financial Protection Bureau (CFPB) and tools from lenders like Rocket Mortgage and platforms like Bankrate make it easy to generate and study your own amortization schedule. The Truth in Lending Act (TILA) gives you the legal right to receive full disclosure of your total interest cost before you close.

Whether you choose a 30-year loan for payment flexibility, a 15-year term for faster equity accumulation, or a government-backed product through FHA, VA, or Ginnie Mae, the same amortization principles apply. The borrowers who understand these principles from day one are the ones who make mortgage decisions that serve their long-term financial goals — not just their monthly budget.