The 28/36 Rule Explained | A Smart Guide for Home Buyers

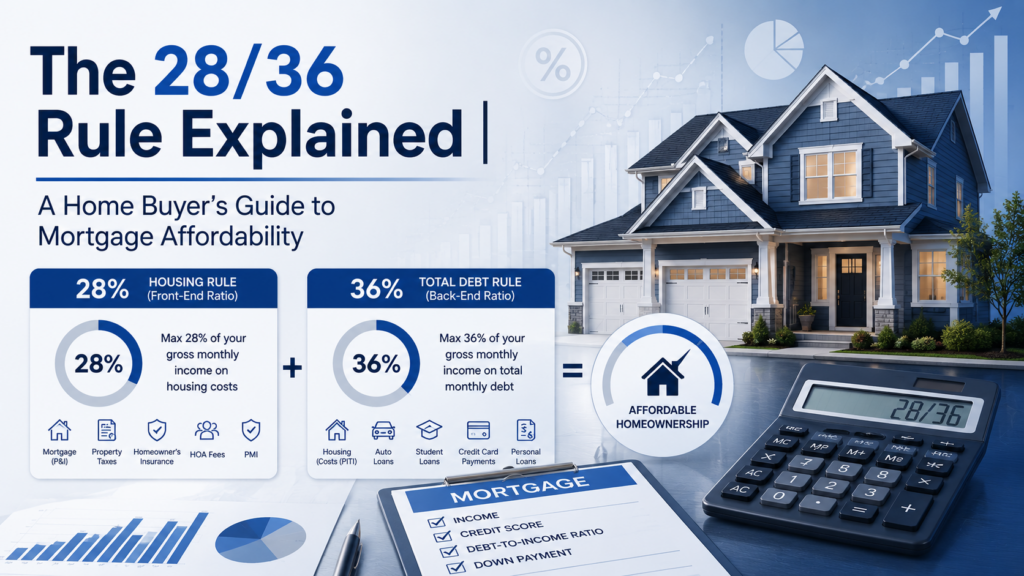

If you’re shopping for your first home or trying to understand how much house you can afford, The 28/36 Rule Explained is one of the most important concepts you’ll encounter. This mortgage affordability guideline gives home buyers a clear, practical framework for evaluating how much they can borrow without overextending their finances. The rule works like this: no more than 28% of your gross monthly income should go toward housing costs, and no more than 36% should go toward all debt combined. These two thresholds — called the front-end ratio and back-end ratio — are the backbone of mortgage underwriting guidelines used by lenders across the United States. Understanding the 28/36 rule explained for home buyers helps you set realistic expectations before you apply, avoid financial stress after you buy, and negotiate your loan from a position of knowledge. This guide covers exactly what the rule means, how to calculate both ratios, where exceptions exist, and how to apply it to your own financial situation. What Is the 28/36 Rule? The rule has two distinct components: The 28% front-end limit (also called the housing expense ratio or household expense ratio) covers principal, interest, property taxes, and homeowner’s insurance — sometimes abbreviated as PITI. The 36% back-end limit (also called the total debt ratio) covers PITI plus all other recurring monthly debt payments, including car loans, student loans, credit cards, and personal loans. These percentages are not laws they are affordability benchmarks grounded in decades of mortgage underwriting guidelines and risk mitigation research. Lenders including Rocket Mortgage, Chase Bank, and U.S. Bank use variations of these thresholds in their qualification processes, though actual limits vary by loan type and lender. How the 28/36 Rule Works in Practice The 28% Front-End Ratio: Housing Expense Threshold The front-end ratio measures only your housing costs against your income. It answers the question: what percentage of your gross monthly income would go toward your monthly mortgage payment? Housing costs counted in this ratio typically include: Mortgage principal and interest (P&I) Property taxes (monthly escrow portion) Homeowner’s insurance (monthly escrow portion) HOA fees (if applicable) Private mortgage insurance or PMI (if applicable) Formula: Front-End Ratio = Monthly Housing Costs / Gross Monthly Income x 100 Example: If your gross monthly income is $5,500 and your estimated PITI is $1,400, your front-end ratio is 1,400 / 5,500 x 100 = 25.5%. This falls comfortably within the 28% threshold. The 36% Back-End Ratio: Total Debt Load Management The back-end ratio takes a wider view. It includes your housing payment plus every other recurring monthly debt obligation. This is the number lenders scrutinize most closely because it reflects your true debt load management burden. Debts included in the back-end ratio: All housing costs (same as front-end) Auto loan payments Student loan payments (minimum or calculated payment) Credit card minimum payments Personal loan installments Any other installment or revolving debt with a monthly obligation Formula: Back-End Ratio = (Monthly Housing Costs + All Monthly Debts) / Gross Monthly Income x 100 Example: Using the same $5,500 income, if you have $400 in car payments, $200 in student loans, and $100 in credit card minimums — your existing debt is $700/month. Adding the $1,400 PITI: $2,100 / $5,500 x 100 = 38.2%. This exceeds the 36% guideline, signaling that debt reduction before applying may be beneficial. Why Lenders Use the 28/36 Rule Lenders use this rule as part of their underwriting process to assess repayment ability and creditworthiness. Research from institutions including the Federal Reserve and academic studies cited by the Consumer Financial Protection Bureau (CFPB) supports the idea that borrowers with housing ratios above 28-30% face higher rates of mortgage delinquency. The rule also aligns with Qualified Mortgage (QM) standards established by the CFPB under the Ability-to-Repay framework, which requires lenders to verify that borrowers can reasonably afford the loans they originate. How to Apply the 28/36 Rule: Step by Step Follow these steps to calculate your own front-end and back-end ratios and determine where you stand relative to the 28/36 guideline. Calculate Your Gross Monthly Income — Use your pre-tax monthly income. If salaried, divide your annual salary by 12. If self-employed, average your last two years of net profit. Include only stable, verifiable income sources. Estimate Your Monthly Housing Costs (PITI) Get a mortgage payment estimate based on the loan amount, interest rate, and term you are considering. Add estimated monthly property taxes and homeowner’s insurance. Include PMI if your down payment is less than 20%. Calculate Your Front-End Ratio — Divide your estimated monthly PITI by your gross monthly income and multiply by 100. If the result is 28% or below, you meet the front-end guideline. List All Existing Monthly Debt Payments — Write down every recurring monthly debt obligation: car loans, student loans, minimum credit card payments, personal loans, and any other installment obligations. Add Housing and Debt Payments Together — Sum your estimated PITI and all existing monthly debts to get your total monthly obligations. Calculate Your Back-End Ratio — Divide total monthly obligations by your gross monthly income and multiply by 100. If the result is 36% or below, you meet the back-end guideline. Evaluate Your Results — If both ratios are within guidelines, you are in a strong position to apply. If either exceeds the threshold, identify whether paying down debt or increasing income would bring you into range. Factor in Compensating Factors — If your ratios exceed the guidelines, consider whether you have strong compensating factors: high credit score (FICO 740+), significant cash reserves, large down payment, or stable long-term employment. These may allow lenders to approve ratios above the standard limits. Compare Loan Programs — Different loan types have different official DTI limits. Compare conventional, FHA, VA, and USDA programs to find which fits your ratios best before applying. How Lenders Apply the 28/36 Rule: Variations by Loan Type The 28/36 rule is a general guideline, not a universal hard requirement. Different loan programs apply different debt-to-income ratio limits, and