How Mortgage Amortization Works | A Clear Guide for Borrowers

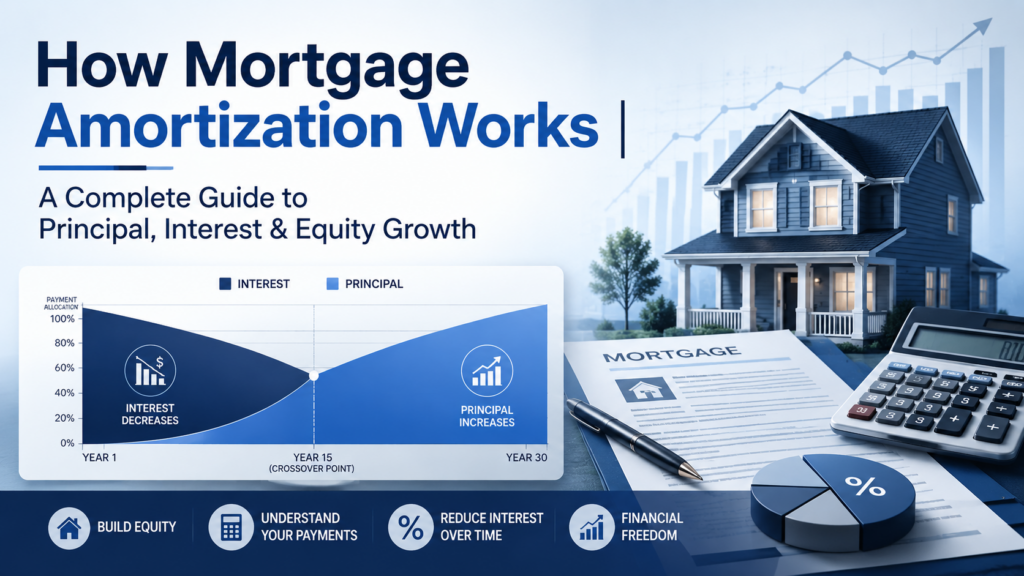

Most homeowners make their monthly mortgage payment without fully understanding where that money goes. The answer lies in how mortgage amortization works — a structured debt liquidation process that determines exactly how each dollar of your payment is split between interest and loan principal across the entire life of your loan. Understanding mortgage amortization is not just academic. It affects how much total interest you pay, how quickly you build equity, whether extra payments make sense, and how refinancing decisions should be evaluated. For first-time buyers especially, grasping this concept before signing a loan changes how you approach every payment you’ll make. This guide explains exactly how the amortization process works, walks through the math step by step, shows you a real amortization schedule example, covers negative amortization risk, and explains how different loan types and strategies interact with the reducing balance method. By the end, you’ll have a clear picture of your mortgage from day one to the loan maturity date. The word ‘amortization’ comes from the Latin ‘amortire’ — meaning to kill off or extinguish. In mortgage terms, it means systematically extinguishing a debt through regular payments using the reducing balance method. Each periodic installment in a fully amortizing loan is identical in size (for fixed-rate mortgages), but the allocation between interest and principal changes with every payment. This shifting allocation is the core mechanism of mortgage amortization, and it has significant implications for equity accumulation and total interest cost. How Mortgage Amortization Works: The Core Mechanics The Interest-Heavy Early Years The most important thing to understand about mortgage amortization is the interest-heavy early years. Because interest is calculated on the outstanding balance — and that balance is highest at the beginning — the first years of your mortgage are dominated by interest payments. On a 30-year fixed mortgage, the typical borrower pays far more in interest than in principal during the first decade. This is not a lender trick; it is a mathematical consequence of how compound interest effects work on a large, slowly declining balance. Example: On a $300,000 mortgage at 7% interest over 30 years, the monthly payment is approximately $1,996. In Month 1, roughly $1,750 goes to interest and only $246 goes to principal. By Month 180 (Year 15), the split has shifted to roughly $1,250 interest and $746 principal. By Month 340 (Year 28), the majority of each payment is reducing the balance. The Reducing Balance Method Explained The reducing balance method (also called the declining balance method) calculates interest only on the remaining loan balance, not the original loan amount. This is why interest costs decrease gradually as you pay down the principal. Each month: Your lender calculates interest by multiplying the current outstanding balance by the monthly interest rate (annual rate / 12). The interest amount is subtracted from your fixed payment. The remainder reduces the principal balance. The next month’s interest is calculated on the new, lower balance. This cycle repeats every month until the balance reaches zero the loan maturity date. Payment Allocation Over Time Payment allocation describes how your fixed monthly payment is split between interest and principal at any given point in the loan term. In early years, the ratio is heavily weighted toward interest. In later years, it shifts heavily toward principal reduction. This pattern explains why: Selling or refinancing in the first 5-7 years means you have built relatively little equity through principal payments. Making even one extra principal payment early in the loan has an outsized impact on total interest paid. The straight-line vs declining balance distinction matters most US mortgages use the declining balance method, not a straight-line split. Equity Accumulation Through Amortization Equity accumulation through amortization is the gradual increase in the portion of your home you own outright. Your equity is the difference between the home’s market value and your outstanding loan balance. Amortization builds equity slowly at first and faster later. However, equity also grows when home values appreciate — which is separate from the amortization process. Falling home values can reduce equity even when you are making payments on time. Understanding the pace of equity accumulation helps borrowers decide when to refinance, whether to make extra payments, and whether a home equity loan or line of credit is accessible. The Mortgage Amortization Formula The fixed monthly payment for a fully amortizing mortgage calculator using this standard formula: Example calculation: $300,000 loan, 7% annual rate, 30-year term P = $300,000 r = 0.07 / 12 = 0.005833 n = 30 x 12 = 360 M = 300,000 x [0.005833 x (1.005833)^360] / [(1.005833)^360 – 1] M = approximately $1,996 per month Over the full 360 payments, total payments equal roughly $718,560 — meaning the total interest paid on this loan is approximately $418,560. This illustrates the compound interest effects of a long-term mortgage and underscores why interest rate and loan term decisions are so consequential. The Truth in Lending Act (TILA), enforced by the Consumer Financial Protection Bureau (CFPB), requires lenders to disclose the total interest you will pay over the full loan term in your Loan Estimate and Closing Disclosure documents. Review these figures carefully before closing. How to Read and Use a Mortgage Amortization Schedule: Step by Step An amortization schedule is a full table showing every payment from loan origination to the loan maturity date. Here is how to read and use it effectively. Obtain Your Amortization Schedule — Request your full amortization schedule from your lender at closing, or generate one using Bankrate’s mortgage calculator, Rocket Mortgage’s online tools, or Microsoft Excel Amortization Templates available from Microsoft’s template library. Identify the Four Columns — Every amortization schedule has four core columns: Payment Number (or Date), Beginning Balance, Payment Amount (broken into Interest and Principal), and Ending Balance. Locate these